Hi,

how do you fund an IB account when you only have a European bank account with (IBAN/SEPA) ?

What are your experiences with IB ?

Best regards

Hi,

how do you fund an IB account when you only have a European bank account with (IBAN/SEPA) ?

What are your experiences with IB ?

Best regards

Best of the best I would say. Use n26 Bank to sent EUR SEPA to IB Account.

IB have EUR account too. So from there you can exchange to whatever currency/stock exchange you want to trade.

I use TransferWise. Works great!! n26 is the other choice, but I like transferwise better. n26 is a real bank and has tax implications, as they turn your name into the country where you have your registered address so that the country can tax you, Transferwise is not a real bank and does not have to share your info with any countries for tax reasons.

I use IB for my long term investment portfolio, it is definitely the best and easily has the most options as far as different stock markets and products go. The software is not the most user friendly but once you learn everything its great to use and really does give you a high level of control. Another honourable mention that I have used is SaxoGlobal - also wide range of markets, good rates, easier to use than IB but for trades in large amounts they can have some predatory practices which is why I stick to IB.

Good luck!

Most important thing is the profit.

Ib is a rare broker who gives you best price like Fidelity, although most of brokers give you higher price for bid.

Its margin interest is always lowest as well.

So you can get profit easiest with IB platform among any other brokers.

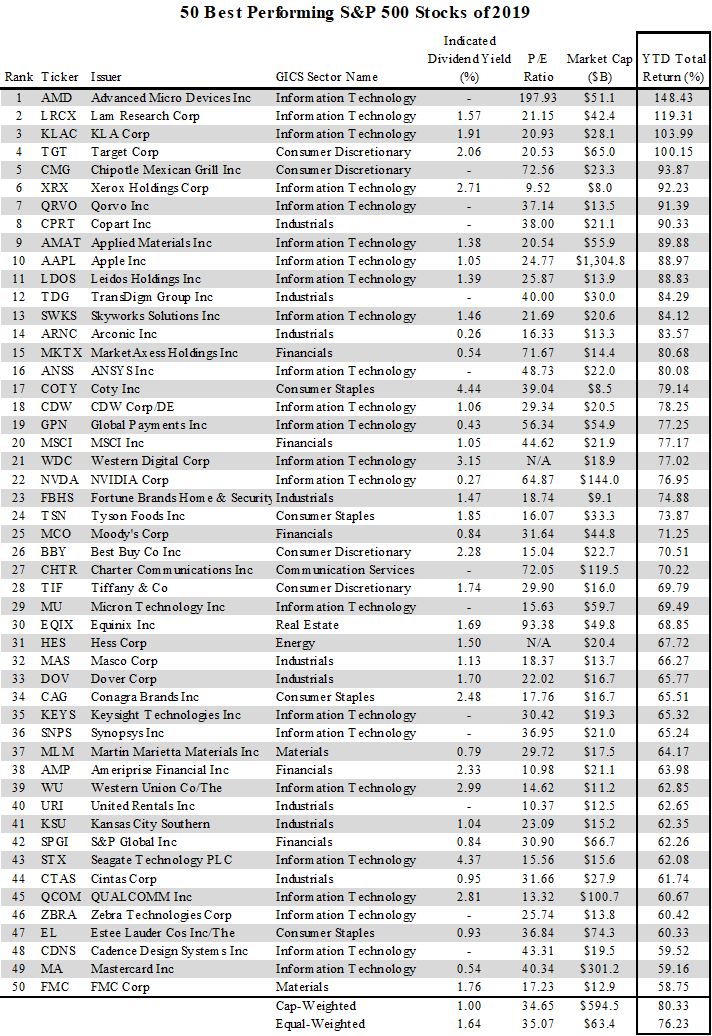

Here is a list of top 50 stocks in NYE. https://static.seekingalpha.com/uploads/2020/1/3/1112099-15781019865672612_origin.png

You could chose some of these for your portfolio that will overcome most of investment, funds, derivatives, etc. Especially, after the next recession or decline of NYX / anti-Trump war.

@65000Tarbes where are you getting this information from? TransferWise, as well as any investment broker you invest with also have to report your end-of-year holdings to your country of residency under AEOI/CRS. It’s not just for “real banks” as you state.

I don’t think it’s a good strategy to look at whichever companies did best last year and just buy those. Google “mean reversion”. Of course, some of them might do well this year as well, but for others investors might realize that they are now overvalued and their stock price will fall to be in line with their fundamentals—or at least grow more slowly.

To be a bit more on-topic: Interactive Brokers is great, although the signup process is a bit convoluted and it might seem a bit intimidating as a newb. Their phone and iPad apps are relatively user friendly, though. I wrote more about IB and other brokers here.

I know you do not well under stand stock market and cashflow (that is capitalism) as you say “It might”, you do not need to say you think, because I know what you would like to say before you say something. I present the list to whom interested in stock market not for index investers like you. The list is among SPY, which performance is at least as you know, one of the best index of NYX, always shows much better performance than most of funds and investments and even hedge funds. The price, PER, of growing company is always high so that you are scared. But for example a company’s PER is 300 for five years and grow 800%. The business of those companies is always open for anyone, and revenue and cashflow you can easily know it through internet. NYX comittee and professional investers and media and government checks up those companies instead of you, so that it is low risk and high return investment for long term.

If you have no idea, you simple dart at the list and invest them, for example 10 stocks, that will give you better performance than most of professional fund managers for long term investment. All you need is buying growing companies in the list and keeping it as long as it grows. For example, if you bought AAPL (in the list) 20 years ago at $5, you now have more than 6000% without doing anything.

This is for people who are interested in stock market, not for complaints and if you are not interested in it, pass through it.

How did you fund IB with Transferwise? AFAI, Transferwise will not bear your name as the sender while doing a transfer, which result in the brokers take it as a suspicious third party deposit.

Your name will typically show up when you do an outbound transfer from TransferWise, at least for EU/SEPA and US/ACH transfers.

Hi Thomas,

Interactive Brokers sure is a good option in terms of fees and features, but I am not so sure the advantages to global accounts aren’t a bit overstated. I have just signed up and was very easily approved, but the fact of the matter is that I am a digital nomad that stays less than 6 months in any given country. Brokers require a fixed address -after all, they have to report gains. I am not so sure the “don’t ask, don’t tell approach” is safe, and I wouldn’t want my funds blocked.

Do you think someone in my circumstances would have issues working with IBKR, and are there better brokerage options for people such as myself?

Thank you so much.

In my experience they tend to ask questions if you add e.g. a tax number from a different country than your listed address, etc (or vice versa). As long as you don’t update your account with conflicting information I think they’d be unlikely to ask questions.

I think very few (if any) financial institutions would be OK with you saying you don’t have a fixed address (or a tax residency).

Frankly there probably aren’t brokerage options at all, if you are not going to accept don’t-ask-don’t-tell. If you have no tax residency, it is hard to apply KYC rules to you, which makes you a massive red-flag, on top of the “so where are we supposed to report your earnings”. You probably are better off just opening the LLC or such - if you can manage to get it past KYC given that they won’t be able to establish substantiaive ownership.

(There are probably options if you have real money. Or you might choose a low-tax locale to claim residency and use that as your base even if you aren’t staying there. Though then you might have issues getting access to product.)

Transferwise is not a real bank, no. However it is a registered, incorporated money transfer institution duly registered with the appropriate tax authorities in each locale. They don’t talk about it per se, but you can find this information if you dig hard enough.

In the US, there is a different type of entity, I forget the official name (and it will vary per state), but it is a type of institution that is regulated by the banking authorities in each state (since banking is a state activity not a federal one). It’s the same license that is used by Western Union.

So while it’s not a bank per se, it operates under many of the same regulations as banks do.

Indeed, at the end of the day, Wise is just a low-fee fintech-enabled Western Union, if you think about it. They just aim at different markets.

Now, since it doesn’t pay interest and therefore does nothing that would create “income” that would need to be reported, it doesn’t have the tax reporting obligations. And since your “balances” are really little more than “store credit” (again, I’ve read into it extensively - that IS how it’s handled from a regulatory standpoint - your balance is a claim against Wise for future services, but that’s it, you just hope they’re good for it, you have very little recourse), there is no bank account requiring reporting along that line. So I would agree with your statement. That doesn’t mean it’s not recording and sharing information or subject to KYC or BSA regs, so your privacy here only goes so far.

(I could provide chapter and verse on this, but I dug into it a while back and don’t care to repeat the exercise. I also speak here about the US entity. It may operate differently in other countries.)

Transfer wise is not a bank but your usd is routed through Evolve Bank and Trust which is a bank. It’s foolish to think they won’t have the same reporting requirements for usd.

Well, sort of and not sort of. The differentiator is that you don’t have an account at the bank, wise does.

if you have a debit card then you do, but it’s a debit card account, with the bill being paid by the wise corporate entity. The IBANs are done in a funny way such that while it’s “unique to you” it’s not really “yours” - again, it’s forms of “store credit”.

(I use this term very loosely - it’s flawed, but it’s the closest analogy I can think of. It should, however, give you a sense of your situation when it comes to the safety of your cash if you choose keep a balance there.)

There are some docs out there where they do explain the mechanics in detail. It’s interesting stuff if you’re into it.

My point was that since there is no interest or other income, there’s no tax so there is no reason to report anything. Broadly, you are correct - BSA certainly applies so someone’s still watching your funds flow around and assuming any real secrecy is naive.

It’s a good analogy. I think if I was a compliance officer at the bank, I would be sweating a little the way it is structured.

Hi Thomas,

Yes, I tried to open an account with Firstrade this week and it was only approved after I provided a phone number from the registered address country, so you make a good point there. IBKR approved the account too, I just want to make sure I don’t have any issues going forward.

I actually have two broker accounts, one is eToro and they just didn’t care when I asked them about these matters a couple of years ago. The other, I hardly manage actively but I have a decent balance there and closed a couple of positions last year, so I thought I would ask how they handle this. The guy said “We have yet to provide information to any tax authority in regards to any client until today”, so I guess I shouldn’t worry too much about this, and any profits should be in the 3 to 4 figure digits anyway.

So I guess I should not have much to worry about if I just go with the “don’t ask, don’t tell” approach. The registered address is from a family member also, what is the worse that can happen, you know?

Thanks for the help! ![]()

Hi Jeff,

I am registered with two brokers and have just registered with IBKR and Firstrade also, so it’s not like I cannot pass KYC, my concern is that the registered address is from a family member in my home country, not the current address, which is not fixed.

I asked the broker where I have a reasonable balance what happens when I close profitable positions, like, do you report profit of x from client y with tax ID z to the relevant tax authorities just the other day, and the guy said “we have yet to provide information to any tax authority in regards to any client until today”, so maybe I’m worrying too much. I’m not trying to avoid taxes (which in theory I wouldn’t owe without a tax residency), I just don’t want my account blocked on account of crossed incorrect information, like reporting I made 500€ to the Portuguese tax authority when I’m not even a resident.

Actually, I have a tax residency this year and foreign passive income isn’t taxed there, but that expires on the last day of the year.

Do you think I’m making too much of this? My profit from closed positions, which I rarely manage, is in the 3 to 4 figures. I just want to cover myself and avoid trouble.

Thank you for your help!

{kind=link}