I recently read about the Italian ‘special tax regime for inbound workers’ (detailed here).

It’s effectively a tax incentive for people to Italy who haven’t lived in Italy before. If you move to one of the southern states or the islands, 90% of your income is exempt from taxation. If you move to the northern states, 70% of your income would exempt.

Considering the south, this means that only 10% of your income will be taxed, and at the normal rate. As an example, if you earned 60.000€, you’d be taxed on 6.000€, which is only in the first band (23%), so your income tax would be 23% of 6.000€ = 1.380€. I’ve confirmed this is the way it works with an Italian accountant.

The question I have is about whether I will be taxed on the remaining 90% in the UK. I won’t be resident in the UK, but I will be tax resident.

I understand that double taxation agreements mean that the same income isn’t taxed twice in two countries, but I’m not sure what counts as ‘same income’ – is it something like the category of ‘personal income’ (or, as another example, ‘capital gains’) or is it actual payments?

If it’s the latter, then it seems like the UK could claim that I’ve only paid tax on 10% of my personal income and ought to pay tax on the other 90% in the UK.

I’m going to consult an account on this in the UK, since it’s down to interpreting the double tax treaty. But I wondered whether anyone had some insight.

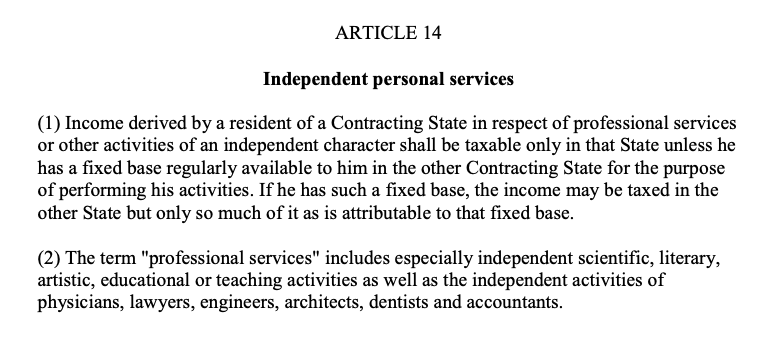

For reference, I think this is the relevant paragraph from the treaty (since my work is as a freelancer software developer). My understanding is that they would use the category approach: my income is from my work as a freelancer, which is taxable in Italy if I am resident there, but not resident in the UK.