It seems to me the real money in banking has always been in interest loans…that’s how most of the super rich got rich…banks and government have always made money together. But these challenger banks seem to just want a percentage of consumer spending with debit cards. If your good at debit cards, why not credit cards? Why not take the new micro-loan ideas learnt over 15 years and combine it with new tech and revolutionize the loaning of money? Finance? It is called fintech…almost seems a misnomer…maybe they should be called “slicetech” as they are now.

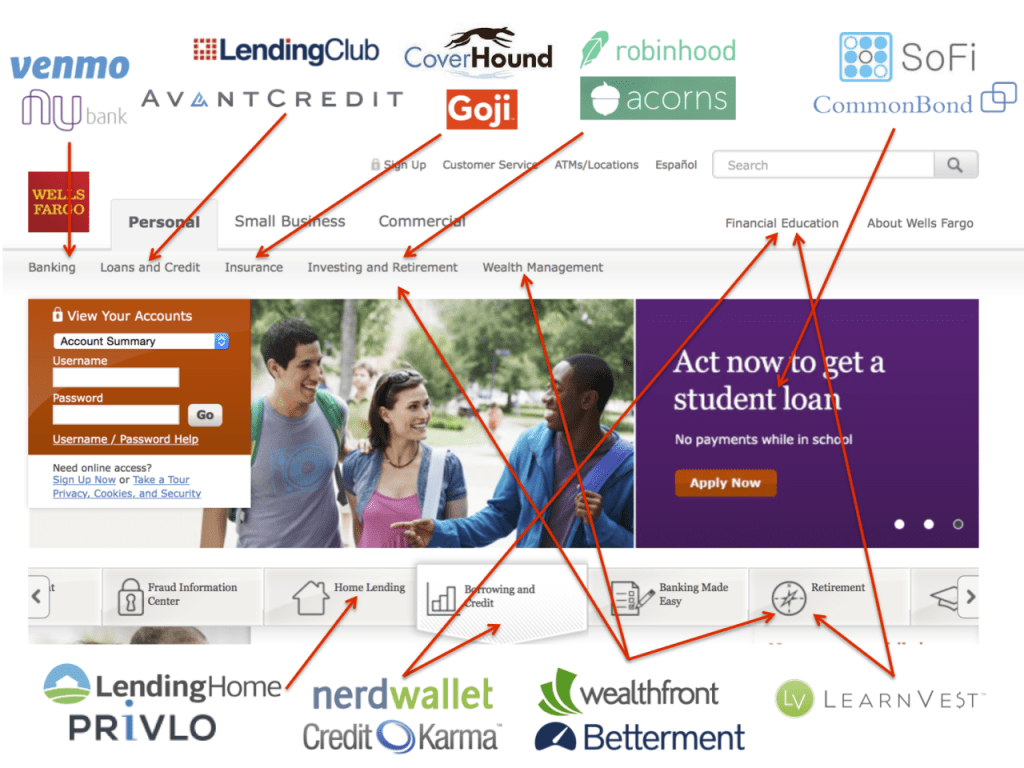

Upon further study I see some are going for loans…they’ve basically broken the banking market into subsections and chosen which one to be in…I guess all hope to slowly expand into the others. Here a great graphic showing all the services/products of one big bank, Wells Fargo, and how each area is being tackled by smaller fintechs…

From the wonderful article: [https://softwareengineeringdaily.com/2020/01/30/whats-behind-the-rise-of-challenger-banks/]

1 Like

Well to my knowledge to provide loans, you have to have different kind of licenses from the ones that are required to provide remittances and e-wallets (like EMI). It’s probably harder to get as well.

Right so probably they get to market with quickest route and then slowly grow and add stuff as they can get it…many use a partner bank…someday get their own bank charter

I’ve been reading about them and there are plenty software companies building the core banking software they need…so they are just compiling stacks of different software and putting it all together…this is cool…but it also gives me pause…they are going to need time to figure out how to run all that stuff consistently…and to keep up with the regulatory side to protect our money…and so many Oops and slip-ups are happening and thus you can find a lot of complaints about them online.

They are definitely “the not yet ready for prime time players” as they used to self identify the cast of SNL.

But for a portion of money worth trying.

True, there is a lot of work in the underlying infrastructure. But usually fintechs are relying on existing banking platforms to offer their services. They’re not reinventing the wheel sort of speak. So a fintech can hold your money but in reality they are sitting in a bank account somewhere and usually are protected by law up to 100k. Even if the fintech goes bust. But I agree, there’s a long way to go to catch up.