My first US creditcard, (a capital one platinum) just arrived in the warehouse.

Can i let the employees open the mail and let them scan the card so i can add it to google pay and start using it? my experience is that mail across the pond takes ages and i wanna start building a credit score before july 18 with the incoming itin changes.

Also: In general for cards that will be churned not kept. is it generally safe to let anytime mailbox scan them and shred them? i might just do that for the churn cards but AI Is telling me sometimes they will tell you to send a pic with a passport and the CC as proof.

Bonus: If anyone knows more about these ITIN changes July 18th, can they tell me if i will be affected? as far as i understand it just triggers more mannual checks, which in my case wont be an issue since i now have proof of adress and a credit history.

There is really no right or wrong answers on this and it really depends on your comfort level to allow someone other than you getting their hands on your credit card.

I’ve had someone in the EU open my mail (and scan my credit card and its PIN) before they physically mailed them to me (and I paid extra for fast shipping, for a peace of mind). But only if I can change the PIN afterwards and I trust that my EU mailbox attendant didn’t go out of their way and writing down my card number, CVV and exp date. Most EU card issuers would need you to activate them by sending a 2FA authentication such as SMS to à registered mobile number. US issuers can be hit or miss.

I highly recommend you don’t ask the mailbox people to shred the card. Get it in your possession and activate it.

Thanks for your reply, Its actually an american card though. Im not sure if even asking them to scan in the CVC is legal or against the TOS of anytimemailbbox

Yes, I know you’re talking about an American card (Capital One) which is a very common card. In my EU mailbox they WILL scan the content of an envelope but I’ve given them a POA (Power of Attorney) to do so. If you didn’t sign anything like this with Anytime Mailbox, then you’re correct, they won’t even dare open it.

My advice is to get them to ship it to you immediately. Pay the more expensive shipping fee for a UPS International or whatever Anytime Mailbox offer and don’t take your chance. Credit card skimming is super common in the US and your right is much less than in the EU (where they have much stricter rule). Yes, you’re only liable up to a cetain USD amount but do you want the hassle of having to call customer service to sort this out? Case in point in the EU, they have 3DES scheme whenever you use a credit card online, and not to get too technical, they need to authenticate you before they can authorize the charge. Here in the US? Not really. MAYbe once in awhile they want to send you an SMS (Amex does this), but most often, once someone has your credit card number, exp date and CVV, off they go (shopping!).

And by the way…building credit scores in the US takes time. You’ve already qualified for a US credit card with your ITIN, so go ahead and use it wisely. I thought the Jul 18th change had to do with how you qualify for such card - which no longer applies to you. Churning cards does NOT help with your credit score by the way, sticking with a card (or two) and paying your bills on time (in full, preferably) does.

I did end up letting them open and scan it which they did since im moving soon and i just wanna get the credit reports moving. Because of the move cheap shipping wasnt an option and honestly i didnt feel like paying 40$ for a no perk card.

The card got scanned in and activated fine but was acting weird when i was trying to create a digital card. It asked for another two factor but said my number was unkown? eventhough its the same number that i use for the login 2FA and its a genuine american ultra mobile sim. But no serious problems so far no lock outs or blocks or anything, im waiting a few days before the first charge cause of this weird error cause i dont want the fraud system to kick in. I guess now its just a question of waiting 12 months before chase will accept me. Might run some business cards welcome bonusses in the meanwhile.

Was thinking to just run a 0,15c balance charge to amazon balance monthly so that theres “activity” on it every month since i have no reasons to use it right now. Is that better then just leaving it unused?

Risky move in my opinion to let them open it, but it’s your card. Please do watch your statement closely each month & dispute unrecognized charges immediately.

Sometimes there is a (small) price to pay in order to establish something important in a different country (such as a credit score). I don’t know why your 2FA is behaving weirdly, if you’re 100% sure your UltraMobile SIM is roaming fine in (what country are you in again??) and you have done an SMS test previously. I hope you activated your UltraMobile SIM before it left the US, since it might be what’s needed. Most banks in the US have not embraced 2FA with Google/Microsoft Authenticator yet, still relying solely on SMS. So do make sure your incoming SMS is solidly working.

Charge more than US$0.15 if you want to see some real improvement in your credit report. Go subscribe to the US-based Netflix or any of the subscription service where they don’t send you physical things. It doesn’t have to be every month. Yes, don’t let it go ‘dormant’ or unused.

Two things as an American who has had a CapitalOne credit card before. Choose Youtube over Netflix for a subscription if you want a monthly charge - easier to cancel. Also Capital One security will drive you nuts - they refused international charges for no reason and let suss domestic charges go thru seemingly at random. Be on top of them.

Yeah i would never do that with a permanent card but this card is getting frozen and product changed ASAP. Im in the Netherlands, Login 2fa works fine its just trying to create a digital card, also trying to add to google pay isnt working.. honestly after it locked me out once im gonna stop f■■■ing with it and just manually hit the digits for payments since i dont need this card for anything but credit building. It is kindoff annoying tho i suspect it detects the VPN.

Capital one is gonna be a f■■■ing headache for me anyways now that they went to discover, which breaks my heart since i really wanted a savorone.. the acceptance here for Visa and MC shot up with the death of Maestro (our old debit card system) But amex and discover is still very rare. i found some weird AAA and Kroger cards that can give 5% tho so im gonna try to get those for my grocery spent since my food delivery grocery allows CC.

Right now a big issue is im moving July 1st and buying around 5-6k of new furniture which would be a great MSR contribution to a welcome bonus + i got a friend i trust going on holiday that can put like 5k spent on a card, i got accepted for an Amex Gold buss but they ask for 15k MSR which i cant relaly hit rn in 3 months any ways to get that MSR down? i know its early to get another card but wasting 10k of spend really hurts when some cards or 5k extra spend means 100k miles for that money

Any chance i can get that MSR down by calling them?

Also: should i be usisng one of those credit builder hacks that allows you to put a subscription or something trough it to get extra credit reporting? or is that basically useless?

Im a Revanced user so i dont have these problems (highly reccomend).

Ill probably just put my anytime mailnox on there (is that dumb?) Or my google workspace @ $8 per month

I can’t even begin to imagine. You’re getting a bonus. You want them to give you that bonus and you not even do the minimum spend for them to try to make something back on you?

I doubt those credit builder hacks work meaningfully.

I also don’t really even think it matters if you spend on a card.

you need to spend a bit on a card for a bank to keep it open for you at all.

it matters just what the cost/benefit ratio is for the card in the first place.

if the card is just one of many cards from that bank, they aren’t going to care that much if you keep the other cards. I had one card I spent $0 on for like 5 years before they even noticed and killed it. A once a year charge would have done it.

if it’s a card from a bank and it’s your only card with them, they’re likely to care a lot if you use the thing because there is a hassle factor to your existence at all.

your credit score is fundamentally an aggregate - and it’s not just about score, even.

do you pay on time?

do you have different types of credit? having a mortgage or other bank loan matters because it creates more footprint. And note getting those bank loans is going to depend on a lot more than just the numeric score.

do you have reported employers?

do you move a lot? changes of address on a frequent basis are a red flag.

do you spend a fair bit overall?

It kinda also just depends on what you intend for out of the credit score.

Also, though I have no proof on this, having only foreign spend on a card is likely problematic, especially a premium card with perks. The ecosystem only works because they get to screw merchants to pay for the perks. If all your spend is in the EU where interchange is capped, they lose money on you. Now of course there are people that game the system all the time - you get a CSR but only use it for hotels, you get an AMEX Platinum and only use it for flights, etc, and they lose money on those people, mostly (though they get the high annual fee). Those people are a minority and it comes out in the wash. They’re getting 4-5% on interchange fees from the merchant so they’re flat on the deal net-net anyway. EU charges capped at 0.2-1.5% (https://www.mastercard.co.uk/content/dam/public/mastercardcom/eu/gb/Other/MC2__rates.pdf) mean you are a total cash sink. You cannot tell me they don’t filter for that.

Haha I’m very well aware of the amount they charge merchant as i am a merchant myself. It’s 3%+ here in Europe too and as you said the USA is obviously even more.

As far as all spend being foreign:

My ad account for Facebook ads is in usd. As I run an ad agency that will be used alot once I recover from surgery and moving.

The question about MSR was more about procedure with these offers. We really don’t have this system in Europe so I really wouldn’t know what’s possible and what’s not. For instance you would never call a bank for more interest here but calling a phone or electricity company for a lower offer is standard.

I guess my only move now is to waste the vacation and moving spend of 10k and wait untill I have 15k of spend on ads only or qualify for a card with a lower MSR

I don’t know from personal experience of trying it, but I’ve never heard of anyone doing it. You don’t negotiate with the electric company, and the major phone carriers avoid it as much as possible; generally you are either doing a price match (in which case they want to see your bill) or attempting to find some existing discount program, and of course most people don’t do it. Cars are an exception, and it’s one that upsets most people as they more or less end up feeling screwed.

It’s a difficulty I find as an American in Europe - you know people negotiate all the time here, but it’s not in my DNA to know how - and vendors know that, hence all the stories of restaurants jacking prices on Americans and expecting tips and all that, we’re marks.

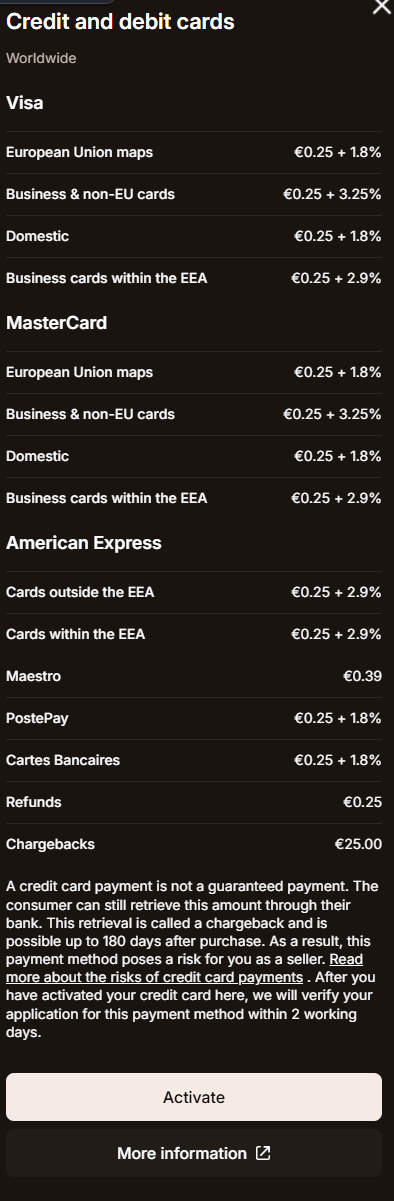

As refference i pulled up some Mollie merchant rates. Im pretty sure these are by far the lowest out of all the payment processors here.

As far as bartering in NL: Its really not okay to do it in person unless your on an actual marketplace. As far as an American tax its not something i have noticed, not like the Farang (foreigner tax) In Thailand for instance. Its more so that certain stores are only visited by toursists not locals cause locals know the pricing is absurd (those weird pirate themed candy shops come to mind) Tipping in NL consists of rounding up the number like paying 85 for a 81$ bill. (but NL is more conservative tipping wise then most counties)

What i more kinda meant is that with customer service/sales/retention employees theres certain “buttons” that you can push to “unlock” a better rate/offer. I wouldnt say its neccesarily common knowledge but its something i picked up when working those positions as a teen.

Oh. That’s including Mollie’s fee, since presumably it’s not working for free. I’m just talking about the straight visa/mc interchange rate, which can be up to 3.15% by itself. However this varies on a per-card basis, as insane as this sounds; if someone swipes a Capital One Platinum, visa can charge as little as 1.2%; if someone swipes a CSR, visa will charge near or over 3%. Stripe charges 2.9%+0.30 swipe, but they can do that because they’re large enough to be able to blend the rate - since most people have Platinums and few have CSRs, they can still come out ahead.

(This is of course a real bone of contention - the Average Joe is effectively subsidizing rich people. But that’s out of scope.)

Oh, business cards aren’t capped, and those start to look more like US rates. Nor are non-EU cards. I guess all that spending adds up enough to drive up the necessary rate.