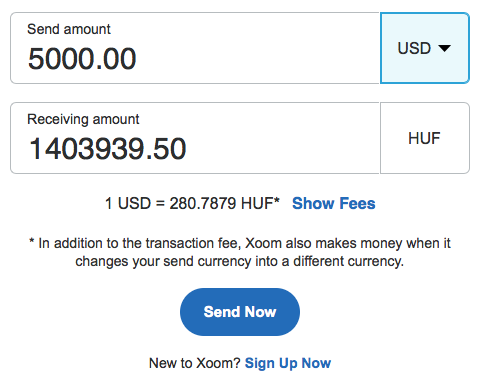

I’ve never seen Xoom being cheaper than Transferwise, even on the USD to EUR corridor where Transferwise is a bit less cheap than when sending European currencies.

Take a 100 USD transfer to EUR today as an example:

Nope. I already have a bank account in the country I am xferring to and so I am depositing in local currency. Bank account to bank account transactions incur 0 transaction fee on Xoom. I checked TransferWise before and that is the reason I use Xoom.

Maybe if you don’t have a local bank account TransferWise is better, but for me it just isn’t.

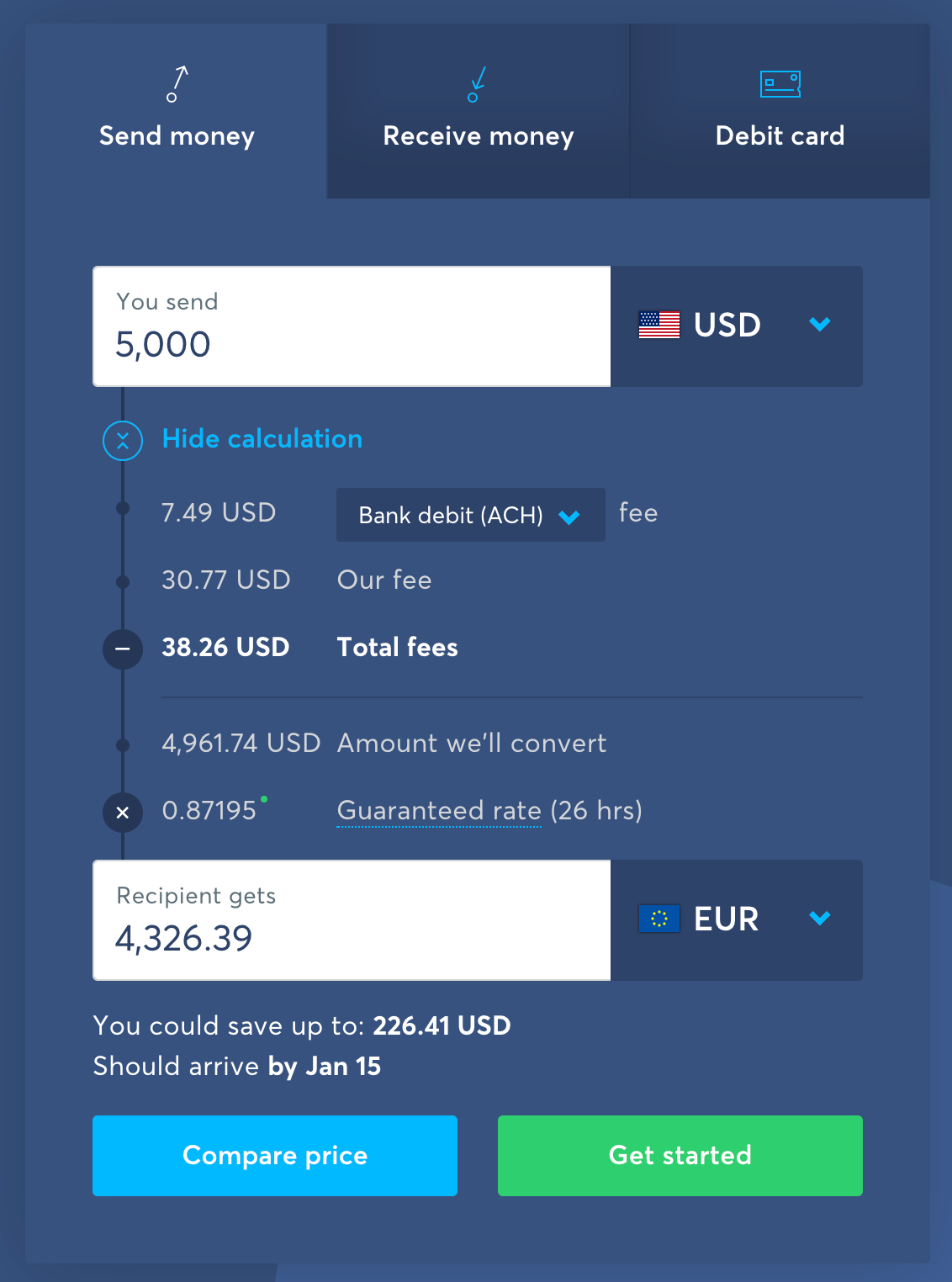

Example, transferring $5,000 US is $46 bucks cheaper with Xoom - based on today’s exchange rates.

Has anyone tried Denizen? I downloaded the app in Sept of 2017 and have been a Beta tester and exclusive user since. They use XE’s previous day end rate for FX rate when I convert USD to Euro, have no Bank owned ATM fee’s, and free transfers between my US, Spanish and German linked accounts.

As an early adopter I have paid no monthly fee for the card (which I have used to withdraw Euro’s in all of the Eurozone) as well as local currency in Hungary, Sweden, Czech Republic and Croatia. www.denizen.io is their website, and they are on both the Apple and Google stores, respectively.

As far as N26, Revolute, Transferwise, etc… I have used them all, and the cheapest and easiest to use has been Denizen. Would love to hear if anyone else has used them, and what their thoughts are, as I did read they are coming out of Beta and will be launching a more Premium product in the coming months that will have a monthly fee. (I have my direct deposit going to my Denizen account because I can then transfer to my US and EU accounts and pay all my monthly bills without hassle and fee’s)

I am talking about transfers to a local bank account, there aren’t any other options with TW.

I wonder where you are getting your rates? It’s currently $25 cheaper to do the transfer you mention with TransferWise than Xoom. $32.50 if your US bank doesn’t charge for wire transfers so you get out of the ACH fee with TW.

I tried to sign up, but unfortunately wasn’t able to since I’m not a permanent resident in either of those countries. On paper it sounds like a great product, so it’s great to hear that have been your experience as well.

It will be interesting to see what their plans will look like in the future, as I doubt the current pricing will be sustainable. But still, it might be worth getting an account now, in case you get grandfathered in to the current price. If I recall correctly, they hinted at something like that, no?

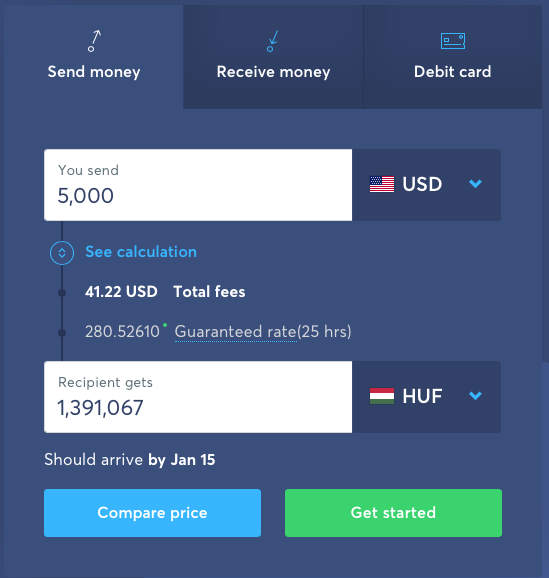

My bad, I saw EU in your first post and assumed EUR. I haven’t checked out all currency pairs, but it seems like at least for USD to HUF of that size they are indeed cheaper. But I wouldn’t extrapolate from USD → HUF and conclude that they are cheaper for all/most transfers to the EU (who after all tend to be EUR or GBP, where TW has the edge).

Bottom line, it’s worth checking with both providers before any given transfer.

Hello, thank you, very useful article. I have an account on Oceanpay, (don’t know if you heard of it) it’s supposed to be an international account. The fees to withdraw from the atm on different countries are high, and sometimes even to use it at some places to pay. Would you recommend to get an account in N26, I’m scared since I don’t really live in Europe, the account in oceanpay is in usd, N26 account only take euros? So would it be more expensive because of the exchange rate?

Hello everyone. I’m going to become Nomad in August 2019. I’m looking for a Bank that is; online, do not need a mobile phone for messages, because I will change country 5-6 times a year, (((Is there any alternative to the mobile phone that can receive and send messages?)))) low deposit rates and ATMs throughout Europe, North Africa and Latin America.I have 2 Nationalities, and utility bills only in this one that I don´t want to use for the identification of the bank. However, my Photo Documents are all up-to-date. I d´ont trust Germany Banks. Maybe a offshore bank would be the best for me BUT I do not want to pay a buck to open an account. I tried to open an account in Monese and Revolut and both didn´t work Revolut wants an associated bank account but i don´t want like so, and only allows to set up the currency of the country where I am currently, the Swiss. I’m finding everything very complicated to fulfill my dream of going to travel 3 years … Someone kindly give me some suggestions please? God bless you

Thanks for the full article, it had widened my views.

I’m italian and I currently live in Japan I decided to go back to the Old Continent (Europe probably -but I’m checking Brexit news- or ) within the year or in January 2020 at the latest.

I have a bank account here and no bank account in Italy, that’s how I ended up reading this article: 99% I won’t take back a residence address in Italy, I may stay at my parents for one or two weeks but I will move to the next country within 20 days max so I am looking for solutions for my money and savings to be moved with me

I was looking at N26 infos and I was excited by it, since it could be the solution for my money to be somewhere in my period of transition between countries, but since I lived here for 5 years I no longer have a residence address in Italy. My parents live there, but legally I don’t live with them anymore so I’m not sure I can use their address. I mean I could use it for the card to be shipped there, but I’m not sure I can use it as the user residence address. And it looks like I need an address within Europe where I result to be living…?

I’m kind of confused. I have the impression I’ll be experiencing a finance no-one-land situation and it even sound less troublesome (though more dangerous) to just withdraw all my money and put them inside my bra as I board the plane back to italy

If you’re not living in an EU or EEA country, you are technically not able to sign up for N26. However, if you sign up using your parents address to receive the card, there shouldn’t be any issues. Your parents address will be sufficient for them to verify your residency in the EU or EEA. Perhaps in the future they will start asking for more detailed address proof (e.g. utility bill with your name), however right now it’s fairly easy. Perhaps they’re turning a blind eye to this workaround to grow more users, who knows.

Afterwards, you should be able to use the N26 account without any issues in Europe and abroad. I haven’t heard of anyone having their account closed for being a non-resident of Europe.

Majority of the accounts closures I’ve read about online have been related to some kind of suspicious activity (e.g. cryptocurrencies, money laundering). So if you use the account for normal spending and don’t do large suspicious transfers and transactions, it should work fine.

I would also suggest signing up for Transferwise if you get the chance since they offer a handy debit card for EU/EEA residents. Transferwise is also easy to sign up for and the card delivery to your parents address is sufficient for address verification. However, if you already have a Transferwise account and wish to change your address, they will require detailed address proof.

This is exactly right. You shouldn’t have any problems signing up with your parents’ address, and then updating it to your British or Irish address once you get settled there.

Note that you’ll get a EUR account in Italy, but if you end up moving to the UK you can just open a Monzo or Starling account there, or close your EUR denominated N26 account and then re-open it a couple weeks later as a GBP account.

Hi Panelinha,

Re the mobile phone thing, I signed up for a virtual phone number (ie it just runs as an app on my smartphone), in my case I used Dingtone to get a US (New York) number for about USD1-2 per year. With this number I can send and receive SMS for my NZ-based and other international services with no real issues so far. Only 1 dinosaur bank insisted on a local number so far. I do have to live with various ads in the app, and the occasional spam phone call from US robo-dialers, but otherwise seems to work ok

I got a question regarding video verification process [for lifting the amount limitations] through Skype or mobile app; As my research in the arranged video call meeting, I need to present the same initially submitted document [ID or pass] again behind the camera [which is fine] and answer several questions.

For the 2nd part do you [or anyone] know what type of questions might be asked [specifically for the case where actual country is out of Europe but the card delivery address has to be within Europe]. shall I be physically in Europe at the time of video call request or I can do the verification in my own non-Euro country first and then request for the card by adding a Euro address of a friend to collect it? anyone has such an experience or information for any of those online banks? [In other words are those video call questions related to the actual place of living or just related to type of account usage or … ]

P.S. Thanks for the great article. This type of information inspires people and change lives. [many people get an opportunity to start or take online business to next level]

I have almost any account (PaySera, N26, CurrencyFair, PayPal, CurrenciesDirect, LeoPay, Revolut, Neteller, Skrill, Tinaba, Monese just opened, and more) but still I didn’t find what I need: a TransferWise alternative. When I tried to add a company to my personal account, something happened and they decided to close my business account and my personal one too, because they were linked. After weeks of emails, they wrote me that I can’t continue to use my personal one. That’s why I am here, looking for an account with both USD and EUR separated bank accounts (with routing number the first and IBAN the second, both under my name). But, at least, I can use also an USD based bank account (under my name) because how to convert currencies is not a problem at all. I am Italian citizen and resident.

Are you aware of a mile-long list of recent complaints of the first bank you recommended (N26) on TrustPilot?

Ranges between benign ones about the customer service, all the way to scary ones about people transferring their entire salaries which were then inaccessible…

@mradovan Believe it or not, N26 has great TrustPilot reviews compared to most banks, even other neobanks. I checked perhaps 10 popular banks now, and N26 had the best score (4/5), along with Revolut, Monzo and Danske Bank (although those still had a larger proportion of 1 star ratings). All other banks I checked had 1-3 stars.

Most of their negative reviews seem to be from people not qualifying for an account or having problems opening one. I’m sure most of those guys would have been OK if they had read this article first. Others seem to be related to compliance related issues, which all banks deal with and are never popular by affected customers.

It doesn’t change the fact that we should take the negative reviews seriously. Still, I’ve worked with many dozens of banks across more than a dozen countries, and my experience with N26 has been much better than with most.

It hasn’t been perfect though, they can be a bit inflexible sometimes (hey, they are German after all—no offense, German friends ). In my case they are refusing to convert my N26 Business account to N26 Metal (which I would like to review to share my experience here) or any other “personal” account. Probably it’s because of limitations in how they have set up their backend, but it’s still annoying.

But in all I think their customer service has been great. Usually they reply instantly or within a few minutes on the chat. I chatted with them yesterday to get my investment module activated, and I had someone helping me in 2 minutes.

I agree I’ve been using N26 for a year now and I really like the app. Even if I have been overcharged when making payments or sometimes double payments N26 always refunds me and charge me correctly. Honestly I use it as my main Mastercard and I use it a lot abroad. It cannot beat other banks with transaction cost and currency exchange. I also got Mastercard from Transferwise which basically the same and also have a Neat card which from Hong Kong well at first it seems N26 and NEAT are exactly the same but clearly there is something wrong with NEAT and they are not so trustable as N26 which has been approved by the Germany Banking association.